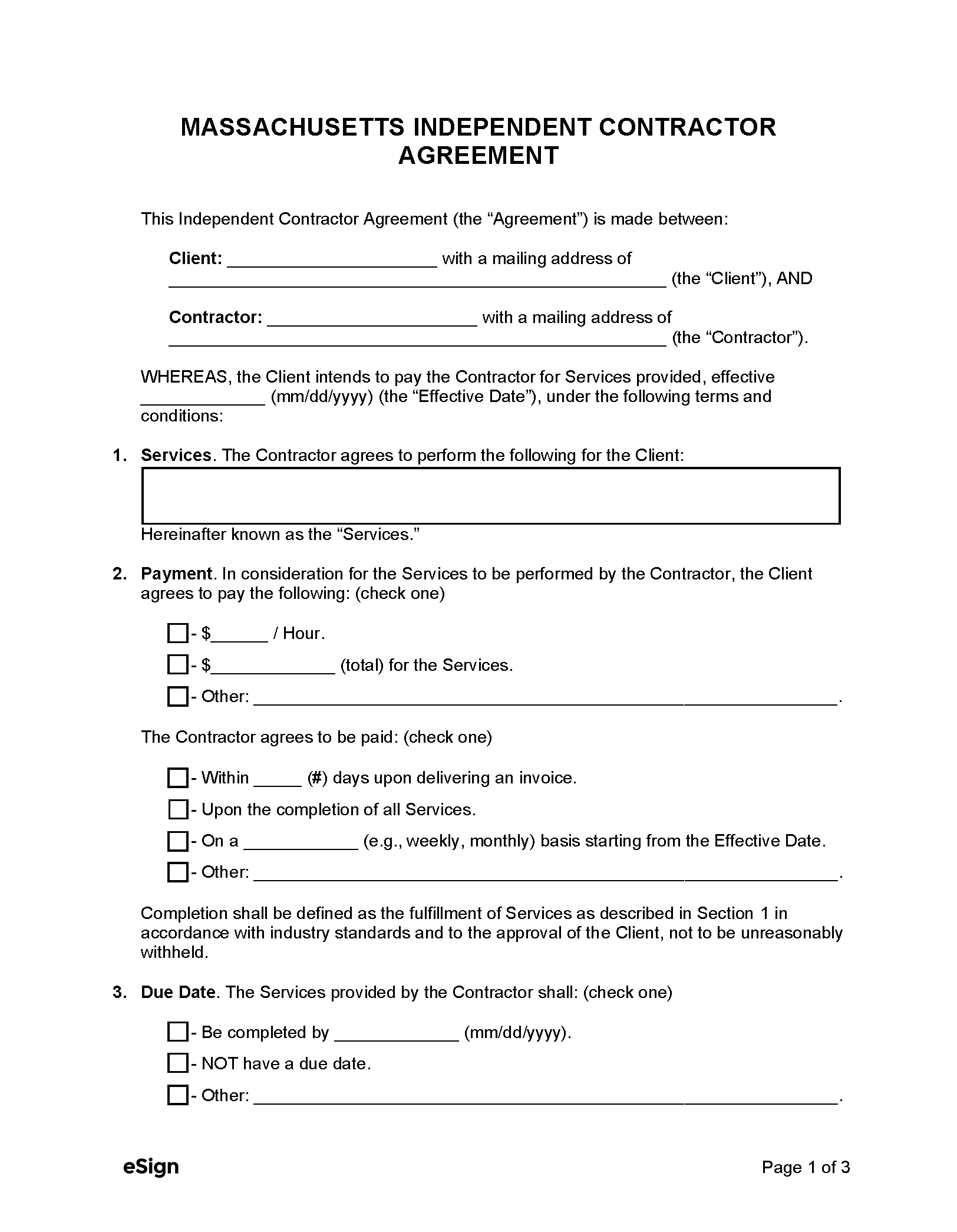

The fresh new valuation payment is actually a fee recharged by a good valuer providers toward work it carry to complete. In this instance, the lending company might have been inquiring these to over good valuation declaration.

They’re going to capture a few photo, measurements, and several of one’s Income and buy Arrangement Layout webpage backup. For folks who did a repair into the home, you might need to support they into power recognition and you can designer concept.

This new valuation statement fundamentally usually explore the true market value out-of the house and some excuse into the property to support such really worth.

Upcoming, an enroll and you can Top-notch Appraisal usually to remain the latest valuation declaration and you may https://paydayloancolorado.net/niwot/ yield to the bank for additional opinion.

Bear in mind, often the significance in the valuation declaration may not match the 1st Market price. Apparently, the situation occurs when the latest banker mistakenly interprets all the details given vocally of the consumer. Or the customer himself considering the wrong suggestions on the banker.

When this occurs, the bank will re also-assess the instance, and you can brand new loan acceptance would-be recognized. Usually, the mortgage matter was slash lower. And that, the money-aside would-be lower.

Basically, brand new valuation commission is approximately 0.50% on brand spanking new loan amount. If you like a precise number of the fresh valuation payment, you could inquire the cost of a good banker.

A financial control percentage was a charge recharged from the a financial to own handling the application. Usually, the new operating fee was recharged once you recognized the financial institution give.

Particular banking institutions may use another type of identity such as for instance a free account set up or opening account charge, nevertheless however involves an identical, and that a fees one charges by the financial and you will an installment you have to pay.

5. Financial Cutting Label Promise ( MRTA ) ( Optional)

Financial Cutting Label Guarantee ( MRTA ) are insurance which takes care of the latest debtor in the eventuality of demise otherwise overall long lasting impairment (TPD).

Whenever unexpected points happen, per se the new demise otherwise TPD; below Home loan Cutting Label Promise ( MRTA), the insurance coverage organization will cover brand new an excellent mortgage.

Based on how much you purchase the mortgage Reducing Name Guarantee ( MRTA ), he has got a drawing you could refer to. New visibility entirely follows brand new diagram.

Into the diagram, he’s got rules year and you may share covered matter toward remaining, stop Worth, and you may Avoid off rules 12 months off to the right.

This is the attempt of one’s Financing Agreement Quotation

You always have the choice to determine the exposure count and you may visibility many years; it’s not necessary to get full dental coverage plans. Seek the advice of your own banker or insurance broker.

The cost of Home loan Cutting Term Guarantee ( MRTA ) is normally a single-of matter. You could will spend of the cash otherwise financing with the mortgage.

The bank advised anyone purchasing Home loan Reducing Title Promise ( MRTA ). Normally some body order it by the glamorous Mortgage attention rates promote.

If you buy a mortgage Reducing Name Warranty ( MRTA ), the financial institution deliver straight down Mortgage interest rates in comparison so you can an individual who will not.

Mortgage Cutting Name Assurance ( MRTA ) prices hinges on the fresh new insured age, publicity number, financial interest rate, gender, and you may years of exposure.

Also, paying actions such spending that have cash or fund on the financing will increase the borrowed funds Cutting Identity Warranty ( MRTA ) insurance premium. Always, when you loans MRTA on financial, the new advanced may be pricier.

If you enjoy this informative article, feel free to express this particular article together with your friends and family. And that i view you in the next that.